India's AI infrastructure market is entering the largest capital deployment cycle in its history. Global hyperscalers are projected to invest $660–750 billion+ in 2026, with roughly 75% directed toward AI infrastructure. Enterprise AI infrastructure spending alone reached approximately $18 billion in 2025, representing nearly half of total enterprise AI investment.

But behind the headline numbers, the data reveals a more complex picture. India's data center capacity has quadrupled in five years, yet GPU availability remains import-dependent. The country has crossed 262 GW of renewable capacity, but coal still supplies 70% of actual generation. AI workloads are scaling at 25–35% CAGR, while frontier talent grows at only ~15% CAGR. And despite 1.25 lakh vacant industrial plots, infrastructure-ready land remains scarce.

Methodology

This analysis is based on the Ellenox AI Infrastructure Cycle India strategic research report published in June 2026. The report synthesizes data from government sources including MeitY, MNRE, CEA, and PIB; industry bodies such as NASSCOM and JLL India; and global research firms including Gartner, McKinsey, and IDC.

Unless otherwise noted, all figures reflect the 2025–2026 baseline with projections extending to 2030–2032. Currency conversions are preserved as originally reported.

Quick Stats: India AI Infrastructure at a Glance

- Operational data center capacity: ~1.5 GW

- Planned capacity by 2030: 4–5 GW

- Installed power capacity: ~524 GW

- Renewable capacity: 262+ GW

- Stranded renewable capacity: 50+ GW

- AI/ML workforce: ~2.75 million professionals

- Core frontier talent pool: 600,000–650,000

- GPUs onboarded (govt frameworks): 38,000+

- Fiber backbone: 4.24 million route-km

- Subsea lit capacity: 309 Tbps

- 5G BTS deployed: 5.18 lakh+

- AI/ML transactions (India H2 2025): 82.3 billion

- 7-year spending forecast (2025–2032): ~$50B → ~$265B

- Data center build cost: ₹40–60 crore per MW

- Industrial power tariff: ₹7–10 per unit

- Captive renewable cost: ₹3–4 per unit

- Data center PUE: 1.4–1.6

Global AI Infrastructure Spending: The $660 Billion Context

The AI market is no longer driven by models alone. By 2025, infrastructure reached near-parity with applications, with $18 billion in enterprise infrastructure spend versus $19 billion in applications. Gartner projects $2.52 trillion in total AI spending in 2026, a 44% year-over-year increase.

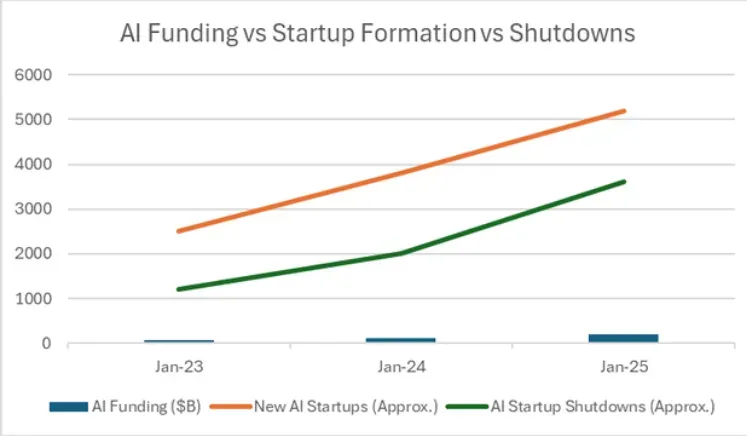

Venture capital has followed aggressively. AI startups raised approximately $114 billion in 2024 and $202 billion+ in 2025, capturing roughly 50% of global VC funding. In 2025 alone, AI accounted for 61% of total global VC investment (~$258.7 billion). Early-stage intensity has also increased, with 40%+ of seed/Series A rounds now exceeding $5 million.

However, failure rates are rising just as fast. Approximately 5,600 AI startups shut down across 2025 to early 2026, implying roughly 40% failure rates even among funded companies. Supply remains constrained: NVIDIA controls approximately 90% of AI accelerators, with data center revenue rising from $35.6B → $51.2B within three quarters. GPU lead times now extend 36–52 weeks. HBM memory is effectively sold out through 2026, and severe shortages persist in advanced packaging (CoWoS).

McKinsey & Company estimates $5.2 trillion in data center capex by 2030, making this one of the largest investment cycles of the decade. The message is clear: capital is scaling rapidly, but so is failure, signaling a shift from growth to selection.

India Data Center Capacity: From 375 MW to 5 GW

India's operational data center capacity expanded from approximately 375 MW in 2020 to roughly 1.5 GW in 2025, with projections of 4–5 GW by 2030. A record 387 MW was added in 2025 alone, reflecting a 103% year-over-year increase over 2024 additions. This acceleration is being driven largely by hyperscaler and AI infrastructure demand, supported by:

- 5G deployment

- Cloud expansion

- Enterprise digitization

- Government-backed compute initiatives

Major hubs include Mumbai with roughly 25%+ market share, followed by Chennai, Delhi NCR, Hyderabad, and Bengaluru. Total hyperscale build cost ranges from ₹40–60 crore per MW, with EPC costs at ₹5–8 crore per MW and cooling infrastructure adding ₹8–15 crore per MW. AI-ready racks now cost ₹8–12 lakh each. Cooling systems alone carry a 20–30% additional premium for AI-ready environments.

AI-ready racks demand 10–20x higher power than traditional deployments, with density reaching 30–100 kW per rack compared to legacy infrastructure. India's average data center PUE sits at approximately 1.4–1.6, significantly above global hyperscaler benchmarks of 1.1–1.3. This efficiency gap represents a major cost optimization opportunity, particularly as energy accounts for 30–40% of total operating expenditure.

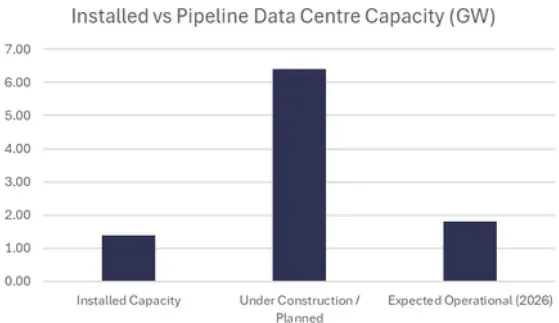

The installed versus pipeline picture shows approximately 1.4 GW currently operational, while another 6.4 GW is under construction or planned. The market is rapidly shifting from traditional cloud infrastructure toward AI-first infrastructure, where facilities require significantly higher power density, advanced cooling systems, and GPU-ready environments. Modular data centers are emerging as a major trend due to lower deployment timelines of 6–12 months versus 18–36 months for traditional builds.

Power and Energy: The 524 GW Foundation and the Coal Paradox

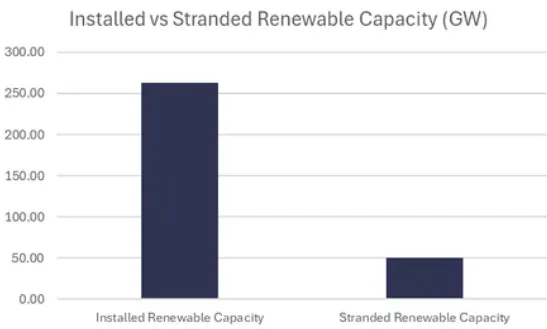

India reached approximately 524 GW of installed electricity capacity in 2026, with 262.74 GW from non-fossil sources, achieving its COP-26 target five years ahead of schedule. Between January and November 2025 alone, India added 44.51 GW of renewable capacity, including 132.85 GW solar and 53.99 GW wind. On paper, India has reached a 50/50 capacity split between coal and renewables.

However, installed capacity does not translate into continuous reliable power. Coal still supplies 70%+ of actual electricity generation. For AI data centers operating 24/7, this creates a major challenge: reliable power availability matters more than headline renewable capacity figures. The gap between installed renewable capacity and actual generation load is widened by a 42% transmission shortfall and the inherent intermittency of solar and wind.

Over 50 GW of commissioned renewable capacity remains stranded because transmission networks cannot evacuate power efficiently. India added only 8,830 circuit km of transmission lines in FY2025, against a target of 15,253 km, creating a 42% shortfall. This mismatch is especially important as AI-ready racks now require 30–100 kW per rack, far above traditional data center requirements. Existing urban grids—particularly in Mumbai and NCR—were not designed for such high-density AI loads.

Industrial electricity tariffs range from ₹6.90/kWh in Karnataka to ₹11.5/kWh in Maharashtra, while captive renewable procurement can reduce costs to ₹3–4/kWh for 20–25 years. Since energy accounts for 30–40% of total data center operating costs, power procurement has become one of the most important financial decisions for operators. The large pricing gap is driving rapid growth in captive solar, wind, and hybrid renewable systems, especially among data centers and industrial clusters seeking both cost savings and energy security.

Large operators such as Nxtra and STT GDC already operate at 60–63% renewable energy integration, demonstrating that partial renewable transition is commercially viable. Behind-the-meter strategies are becoming standard practice:

- Captive solar and wind PPAs

- Battery Energy Storage Systems (BESS)

- Open-access renewable procurement

- Hybrid systems

Battery Energy Storage Systems represent a major opportunity. India's BESS installed capacity stands at approximately 2.56 GW, with a projected $487 billion opportunity from 2025 to 2050. The Central Electricity Authority targets 411 GWh of battery storage by 2032. Without major investments in grid modernization, storage infrastructure, transmission corridors, and captive energy systems, AI infrastructure deployment could face severe power bottlenecks by the end of the decade.

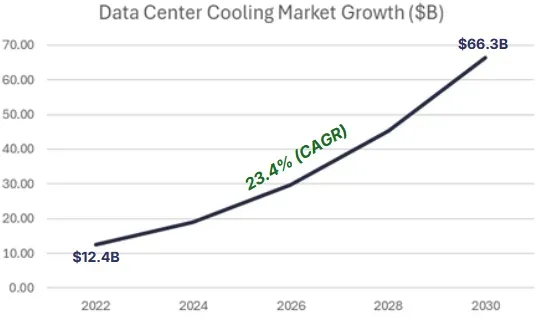

Cooling and Thermal Management: The Hidden $66 Billion Crisis

The global data center cooling market was valued at $12.4 billion in 2022 and is projected to reach $66.3 billion by 2030, growing at approximately 23.4% CAGR. This growth is being driven primarily by AI infrastructure expansion, where a single H100 GPU cluster can generate 20–30x the thermal load of a traditional server.

NVIDIA's H100 SXM5 GPU carries a 700W TDP, while the Blackwell B200 reaches 1,000W per GPU. An 8-GPU DGX H100 server generates approximately 10.2 kW of heat, and fully populated AI racks can exceed 70–100 kW, far above the ~20 kW ceiling manageable through conventional CRAC/CRAH air cooling. The transition toward AI infrastructure is fundamentally a transition toward high-density compute environments where traditional air cooling is increasingly inadequate.

This has accelerated adoption of liquid cooling systems:

- Direct Liquid Cooling (cold plates)

- Rear-Door Heat Exchangers (RDHx)

- Immersion Cooling (single-phase & two-phase)

- Cooling Distribution Units (CDUs)

Immersion cooling is emerging as the most thermally efficient commercial solution, with achievable PUE levels of 1.02–1.05 and support for 200+ kW rack densities. AI-optimized liquid cooling environments are now targeting PUE ranges of 1.03–1.08, compared to the global average data center PUE of 1.58.

However, the sector faces significant bottlenecks:

- Water usage: 100 MW hyperscale facilities can consume 3–5 million gallons/day

- CDU lead times: increased from 12–16 weeks → 40–60 weeks

- Retrofit costs: $2–5 million per MW

- Technician shortage: 35,000+ gap expected by 2026

- PFAS regulation pressure: disrupting immersion cooling fluid supply chains

India also faces climate-related disadvantages including high ambient temperatures and water scarcity in major cities, alongside increasing regulatory pressure around water usage.

Thermal management failures could directly reduce GPU efficiency, facility uptime, and infrastructure ROI. Cooling infrastructure may become one of the largest hidden constraints on AI scaling in India.

Networking and Connectivity: 4.24 Million Route Kilometers and the IXP Gap

India's fiber backbone has expanded rapidly. Total optical fiber route length reached approximately 4.24 million route-km by end-2025, up from 1.94 million km in 2019, making India one of the largest fiber markets globally. Major contributors include:

- Airtel: 400,000+ route km

- RailTel: 63,000+ route km

- BSNL backbone infrastructure

- The BharatNet rural connectivity program

BharatNet alone represents one of the world's largest digital infrastructure investments at approximately ₹1.39 lakh crore (~$16.9 billion), connecting more than 2.14 lakh Gram Panchayats by 2026. This expansion has helped reduce data costs from approximately ₹269/GB to ₹8–10/GB, while helping India surpass 1 billion broadband subscribers.

International connectivity is scaling rapidly. India's lit subsea bandwidth capacity increased from 139 Tbps in 2022 to 309 Tbps in 2025, representing approximately 60% year-over-year growth in 2025 alone. Several major cable projects are expected to add substantial additional capacity:

- SEA-ME-WE-6

- MIST

- 2Africa Pearls

- Jio's IAX/IEX systems

Mumbai and Chennai continue to dominate as India's primary international data gateways.

However, India's digital connectivity ecosystem remains geographically concentrated. The country operates 31 active Internet Exchange Points across 928 member networks, with approximately 60 Tbps installed capacity. Yet these exchanges remain concentrated in only 7 major cities, despite India having more than 168 cities with populations above 300,000. Much of India's domestic internet traffic still routes internationally through hubs such as Singapore before returning to local destinations. Current IXP utilization remains only 5–6%, compared to 40–60% in mature Western markets.

At the data center layer, operational IT load capacity reached approximately 1,500 MW by end-2025. But the long-term challenge is not simply adding capacity. It is ensuring that new infrastructure supports GPU-dense, high-power AI workloads rather than only general-purpose cloud deployments. Inside data centers, AI workloads generate heavy east-west traffic, meaning poor intra-data center networking can leave GPUs underutilized despite high compute investment.

The edge data center market is expected to grow from $627 million → $3.16 billion, at a 19.1% CAGR, driven by:

- AI inference

- Gaming

- OTT streaming

- Fintech

- Real-time applications

Weak Tier-2 and semi-urban interconnection infrastructure could slow edge AI deployment, real-time AI services, and regional digital expansion.

AI Talent and Workforce: The 2.75 Million Person Gap

India's broader AI/ML workforce reached approximately 2.75 million professionals in 2025, reflecting a 55% year-over-year increase. However, the core frontier-level expertise pool remains significantly smaller, estimated at 600,000–650,000 professionals, and projected to grow to 1.25 million+ by 2027 at approximately 15% CAGR.

This creates a structural mismatch: AI demand grows at 25–35% CAGR, while frontier talent grows at only ~15% CAGR. As a result, demand for specialized AI talent is now growing materially faster than supply.

Geographically, Bengaluru remains India's dominant AI talent hub with approximately 478,620 AI/ML professionals, supported by a strong inflow advantage over other cities. Hyderabad and Chennai are also scaling rapidly, while Tier-2 cities are emerging as new talent centers:

- Coimbatore: +72%

- Ahmedabad: +65%

At the infrastructure operations layer, Site Reliability Engineering has become one of the fastest-growing technical disciplines. India currently has more than 23,000 active SRE job openings, with approximately 1,852 new listings added weekly. Demand is being driven directly by hyperscale cloud expansion, GPU infrastructure deployment, and AI operations complexity. The most acute shortage now exists at the intersection of:

- AI infrastructure operations

- GPU thermal management

- CUDA-level debugging

- High-density compute reliability

These are highly specialized skill sets with limited institutional training pathways.

At the physical infrastructure layer, India's data center engineering workforce currently stands at approximately 25,000–35,000 professionals, but will need to nearly double by 2027 to support ongoing capacity expansion. Skill shortages are especially severe among high-voltage power engineers and experienced infrastructure project managers.

India's academic pipeline remains globally competitive. In 2024–25 alone, approximately 390,245 students enrolled in Computer Science and Engineering programs across 1,600+ institutions offering AI/ML specializations. India ranks #1 in AI scientific publications and #5 in AI research talent globally.

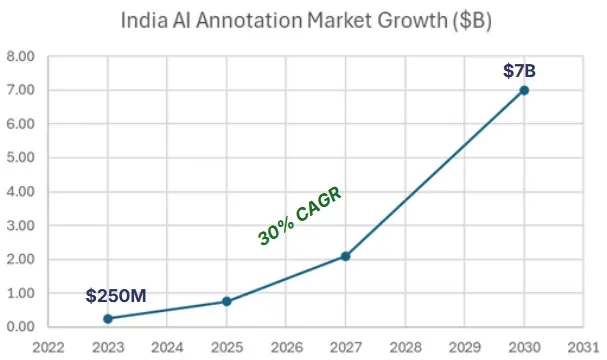

At the data layer, India has also emerged as the global leader in AI data annotation and labeling services. Approximately 70,000 professionals currently work in annotation-related roles, while the market is projected to expand from $250 million (2023) to approximately $7 billion by 2030, growing at 30% CAGR. The global annotation tools market is growing at 20.71% CAGR.

Land and Real Estate: The 137,517 Hectare Myth

India possesses 137,517 hectares of industrial land with more than 1.25 lakh vacant plots across industrial parks and estates. Yet much of this supply remains underutilized because many sites lack critical infrastructure such as reliable power, high-capacity fiber connectivity, transport access, or fast regulatory approvals. The real constraint is not land availability. It is the availability of usable, infrastructure-ready land.

Geography plays a decisive role in land economics. States such as Maharashtra, Gujarat, Tamil Nadu, and Karnataka dominate due to stronger industrial ecosystems, port connectivity, and policy support. Maharashtra alone accounts for approximately 25,000 hectares, making it India's largest industrial land market.

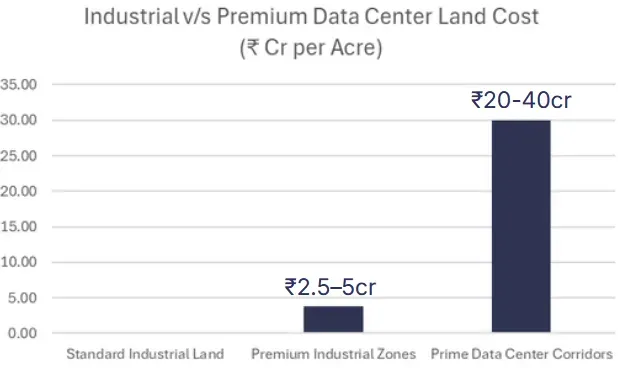

Premium digital infrastructure corridors are experiencing significant pricing pressure:

| Land Type | Price Range |

|---|---|

| Standard industrial land | ₹10–25 lakh per acre |

| Industrial hotspots | ₹2.5–5 crore per acre |

| Prime data center corridors | ₹20–40 crore per acre |

This reflects the increasing value of locations with reliable power access, dense fiber connectivity, proximity to airports and highways, and access to hyperscaler ecosystems.

Compared to global markets, India still retains a strong structural cost advantage. Prime data center land in India is estimated at approximately $100–130/sq ft, compared to roughly $270/sq ft in China, making India increasingly attractive for hyperscalers and global infrastructure investors.

Approval speed is another major investment variable. Basic approvals can now take as little as 2–4 months through single-window systems, but environmental and infrastructure clearances can still add 6–12 months, directly impacting project timelines and capital deployment. Slow approvals, power connectivity delays, fiber deployment bottlenecks, environmental clearances, and urban congestion in hyperscale hubs create a situation where land availability exists, but deployment readiness remains constrained.

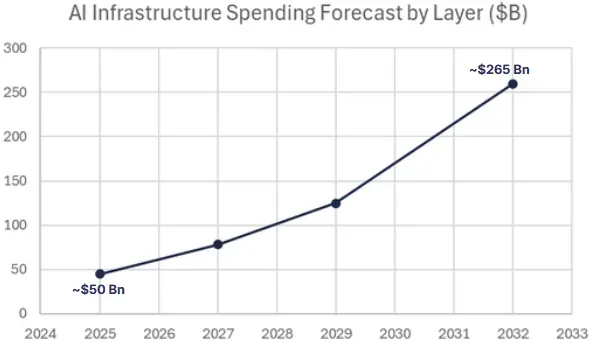

Investment Forecast: The $265 Billion Pipeline

India's AI infrastructure cycle is entering its largest capital deployment phase to date. Over the next seven years, spending is expected to shift from experimentation toward full-scale industrial deployment across compute, energy, networking, cooling, and enterprise AI services.

The 7-year spending forecast from 2025 to 2032 shows synchronized expansion across every layer:

| Layer | 2025 Base Estimate | 2032 Forecast | Implied CAGR |

|---|---|---|---|

| Compute Infrastructure | $8–10B | $45–60B | ~28–31% |

| Power & Energy | $12–15B | $70–90B | ~29–32% |

| Networking & Fiber | $6–8B | $30–40B | ~25–28% |

| Cooling & Thermal | $2–3B | $18–25B | ~33–36% |

| Industrial Land & Parks | $4–5B | $20–30B | ~24–29% |

| Software Infrastructure | $5–7B | $35–50B | ~31–34% |

| Professional Services | $8–10B | $40–55B | ~24–28% |

The total ecosystem is projected to grow from approximately $50 billion in 2025 to approximately $265 billion by 2032. The strongest spending acceleration is expected in infrastructure-heavy segments because AI workloads are fundamentally constrained by physical capacity.

The Bottleneck Gap: Demand vs Supply

The gap between current infrastructure capacity and future AI demand is becoming structurally visible:

- GPU Supply — Import-dependent; severe shortage risk

- Power Grid — Strong generation, but transmission and stability bottlenecks

- Cooling — Mostly air-cooled; AI-density readiness gap

- Networking — Strong backbone, but weak Tier-2 interconnection

- Talent — Large workforce, but frontier skill shortage

- Land — Large supply, but infrastructure-ready scarcity

- Data Centers — Rapid expansion, but AI-grade capacity shortage

The key issue is not lack of demand. It is the speed at which infrastructure can scale to meet that demand. McKinsey & Company projects 156 GW global data center demand by 2030, requiring 125 GW incremental capacity. Colocation vacancy has dropped from approximately 10% → 2%, creating a clear supply shortage.

Risk Assessment: Where the Infrastructure Cycle Faces Friction

Across the AI infrastructure stack, the largest risks are not around lack of AI adoption. They are around compute availability, power stability, cooling scalability, skilled execution, and supply chain control.

| Risk Category | Severity |

|---|---|

| GPU & Hardware Dependency | Critical |

| Power & Grid Stability | High |

| Cooling & Thermal Constraints | High |

| Talent Shortage | High |

| Connectivity Concentration | Medium-High |

| Regulatory Risk | Medium-High |

| Land & Execution Delays | Medium |

| Capital Intensity | Medium |

GPU lead times of 3–7 months, HBM memory effectively sold out through 2026, and severe shortages in advanced packaging (CoWoS) underscore a lack of domestic control. India's 38,000+ GPUs onboarded through government-linked frameworks remain extremely small relative to projected demand from hyperscalers, enterprises, and sovereign AI initiatives. Without domestic advanced packaging infrastructure or fabrication capabilities, India remains vulnerable to global supply chain volatility.

High-density AI racks now require 30–160 kW each, far exceeding legacy infrastructure assumptions. With industrial tariffs at ₹7–10 per unit and an estimated 411 GWh storage requirement by 2032, the sector remains vulnerable to power bottlenecks. PFAS restrictions are affecting cooling fluids, power tariff reforms are shifting economics, renewable procurement regulations are tightening, and data sovereignty mandates are adding compliance layers. Infrastructure planning cycles are long-term, while policy environments remain rapidly evolving.

In the AI economy, resilience and execution capacity may become more valuable than raw technological capability. The long-term winners will be the companies capable of reducing infrastructure friction and controlling bottlenecks across multiple layers.

Credits and Research Team

This analysis is based on the Ellenox AI Infrastructure Cycle India strategic research report published June 8, 2026.

Research and Analysis by:

- Hardik Jain — Project Director

- Rashi Jain — Research Lead

- Yuvraj Singh — Research Lead

- Shikhar Omer — Research Lead

- Suhani Kharbanda — Research Lead

- Devansh Khandelwal — Associate

- Jishnu Narayan — Associate

- Kartik Bhatia — Associate

- Suhani Singh — Associate

- Aryan — Associate

- Chirag Arora — Associate

- Diya Gera — Associate

Primary Sources:

Synergy Research Group, Gartner, Ministry of Electronics and Information Technology (MeitY), Savills India, JLL India, Nomura, IEEFA, NASSCOM, IDC, IndiaAI Compute Portal, Press Information Bureau, Ministry of Power, Central Electricity Authority, Grid-India, PGCIL, CERC, MNRE, Rystad Energy, S&P Global, Astute Analytica, CEEW, Internet Society, DE-CIX India, and industry data from NVIDIA, TSMC, Samsung, AMD, Vertiv, Schneider Electric, Airtel, RailTel, and BharatNet.